The crypto lending sector, which collapsed during the 2022 bear market, has quietly rebuilt itself around a more conservative model, and the recovery is now showing up clearly in the numbers.

Outstanding crypto-collateralised loans reached $73.59 billion by the third quarter of 2025, and platform revenue is forecast to climb to $12.69 billion in 2026, an 18.8% increase on the previous year.

Borrowing rates have also stabilised, with centralised lenders charging between 9.99% and 11.49% for Bitcoin-backed loans in 2026, a tighter range than the volatile pricing that defined the previous cycle.

Unlike the previous wave of lending products, the current generation of crypto loans platforms like AAVE and CoinRabbit are structured around overcollateralisation, transparent risk parameters, and stricter no rehypothecation policies.

The shift reflects lessons from the failures of Celsius, BlockFi, and Genesis, which left depositors badly exposed when counterparties defaulted.

A maturing crypto lending market built on overcollateralisation

The dominant model in today’s crypto lending market is overcollateralised borrowing, where users pledge digital assets worth more than the loan they receive.

The relationship between the two figures is captured in the loan-to-value (LTV) ratio, which determines both the borrowing capacity and the liquidation threshold.

Most established platforms now offer tiered LTV options.

Lower LTV loans carry lower interest rates and reduce the likelihood of margin calls, while higher LTV loans free up more capital but require closer monitoring.

Interest rates across the sector currently sit in a broad band of roughly 11% to 17% on stablecoin-denominated borrowings, with variations depending on collateral type, loan duration, and platform.

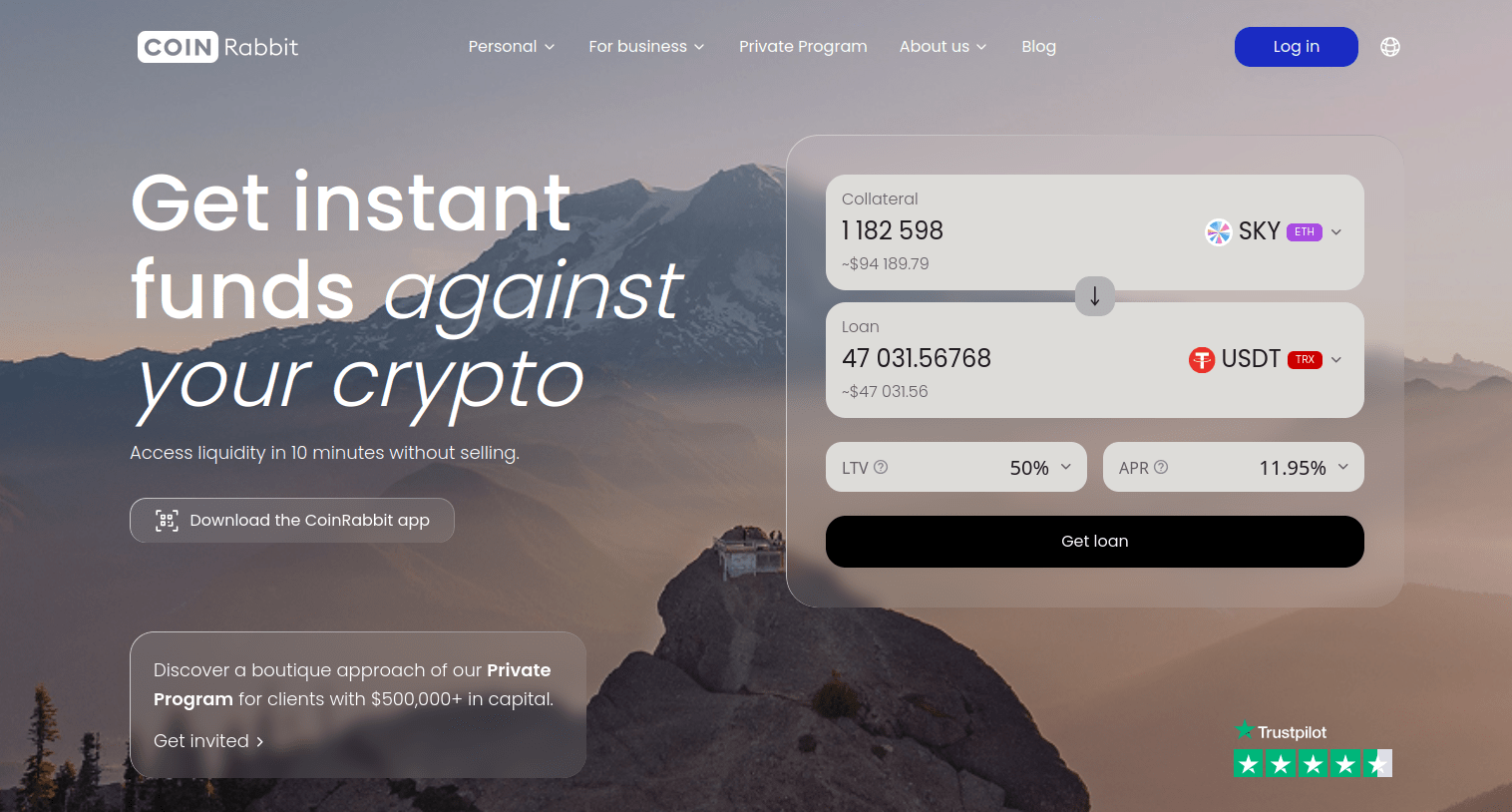

The typical structure offered by established lenders such as CoinRabbit, operating since 2020 and one of the platforms cited in industry analyses of the post-2022 recovery, illustrates how the segment has standardised:

- Tiered LTV options of 50%, 65%, 80% and 90%, allowing borrowers to balance capital efficiency against liquidation risk

- No rehypothecation policy. CoinRabbit adheres to a strict collateral policy, ensuring that user assets are never reused, rehypothecated, or otherwise deployed.

- Liquidation thresholds ranging from 80% to 95%, depending on the loan type

- Both short-term and long-term crypto loan structures, with indefinite-duration options for borrowers who want to avoid repayment deadlines

- Funding times of around 10 minutes once collateral is confirmed

- Real-time LTV monitoring with optional automated collateral top-ups to reduce margin call risk

- Support for over 340 collateral assets, well above the Bitcoin- and Ethereum-only models common in the previous cycle

The diversity of accepted collateral has been one of the more visible changes in the sector.

Where early platforms accepted only the largest assets, several lenders now support hundreds of cryptocurrencies, reflecting a broader recognition that long-term holders are increasingly diversified across the market.

How crypto lenders handle collateral now matters most

Among the structural changes most consequential for borrowers, the move away from rehypothecation stands out.

The practice, common in traditional securities lending, allows the lender to redeploy collateral posted by clients to back its own positions or generate additional yield.

In a stable, well-regulated environment, the risks are manageable.

In crypto, where counterparty failures can cascade rapidly, those risks have proven catastrophic.

A growing number of platforms now operate under a strict no-rehypothecation policy, isolating client collateral so that it cannot be used to fund the lender’s other activities.

The approach reduces yield potential for the lender but materially lowers the risk that borrowers lose access to their assets in the event of a credit event elsewhere in the platform’s operations.

CoinRabbit is among the lenders that have built this policy into the core of their offering, alongside others that have adopted similar segregation models.

The distinction has become a key consideration for institutional and high-net-worth participants, who have grown more willing to engage with crypto credit markets but remain cautious about the structural integrity of any platform they use.

According to official CoinRabbit data, borrowers have collectively accessed close to $1.5 billion in loans through CoinRabbit since its launch, a figure that reflects how the post-2022 lending recovery has concentrated around platforms with conservative custody practices and longer track records.

Stablecoin savings emerge as a yield alternative

Alongside lending, stablecoin-denominated savings products have re-emerged as one of the more durable sources of yield in the crypto economy.

With US Treasury yields easing from their 2024 peaks and traditional money market returns trending lower, stablecoin yields in the 4% to 6% range have attracted attention from yield-focused investors.

Most platforms generate these yields by lending deposited stablecoins to overcollateralised borrowers, effectively recycling the same lending architecture that supports the loan product.

Because the collateral backing the borrowed stablecoins is in volatile crypto assets rather than fiat instruments, the spreads available are wider than in traditional finance.

USDT and USDC remain the dominant stablecoins in this segment, with most platforms supporting deposits across multiple blockchain networks, typically including Ethereum, Tron, BNB Chain, Polygon and Solana, to give users flexibility on transaction costs.

Yields on Bitcoin and Ethereum savings products tend to be substantially lower, often under 2%, reflecting weaker borrowing demand against those assets.

The structure has its limitations: custodial savings products carry counterparty risk, regulatory treatment varies considerably by jurisdiction, and yields are not insured.

But for users who want exposure to dollar-denominated returns without exiting the crypto ecosystem, the segment has filled a clear gap.

Institutional demand drives private wealth management programs

A notable development over the past year has been the growth of dedicated services for high-net-worth individuals, family offices, and crypto-native businesses.

Several lending platforms now operate private programs or institutional desks that handle loan amounts starting at $500,000 and extending well into the millions.

These services typically offer customised lending terms, dedicated relationship managers, cross-collateralisation across multiple assets, OTC execution for large trades, and direct bank transfer support.

The terms tend to be more favourable than retail offerings, reflecting both the scale of the relationships and the lower per-dollar servicing costs.

The trend mirrors the institutionalisation underway across the broader crypto sector, with spot Bitcoin and Ethereum ETFs having drawn substantial inflows since their respective approvals, and corporate treasury allocations to digital assets becoming more common.

Lending against those holdings, rather than liquidating them and triggering taxable events, has become an increasingly important use case.

The remaining structural debate in the sector concerns custody.

Most major lending platforms operate on a custodial basis, holding client assets directly.

This enables faster execution, lower fees, and simpler user experiences, but it requires users to trust the platform’s operational and security practices.

Final thoughts

Regulatory pressure has continued to reshape the landscape, with most established platforms now operating as registered Money Services Businesses or under equivalent licences, implementing KYC and AML procedures, and applying withdrawal limits to unverified accounts.

The platforms most likely to retain user trust as the sector continues to mature are those that combine competitive economics with conservative risk practices, transparent custody arrangements, and a track record across multiple market cycles, a relatively short list, but a growing one.

The post Why long-term holders are turning to crypto lending platforms appeared first on Invezz

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}